I’ve run and advised enough loyalty programmes to see the same debate pop up over and over: should you reward customers with points that convert into discounts, or give them prepaid credits (store credit, cash-like balances) they can spend directly? The right choice isn’t ideological—it’s practical. Points are powerful for acquisition and repeat purchase psychology; prepaid credits are often better at driving immediate revenue and simplifying redemption. In this piece I’ll walk you through a decision test I use with clients—both subscription and one-time-purchase businesses—so you can choose (or decide to test) the right currency for your customers and your commercial goals.

Why the distinction matters

Points feel aspirational. They let you create tiers, gamify behaviour, and nudge longer-term engagement. But they can be abstract and add friction: customers might forget points exist, or not reach the threshold required to redeem. Prepaid credits behave like money. They’re simpler to understand, tend to be spent sooner, and show up in your accounting differently (often as store credit liabilities). The wrong choice can cost you either in unused liabilities or missed opportunities to activate buyers.

Start with the commercial question

Before diving into UX or tech, I ask founders two commercial questions:

If your priority is quick sales and reducing churn in a subscription product, prepaid credits often win. If you’re building a long-term emotional relationship or want to introduce tiers and status, points can be better. The remaining sections turn that intuition into a testable decision framework.

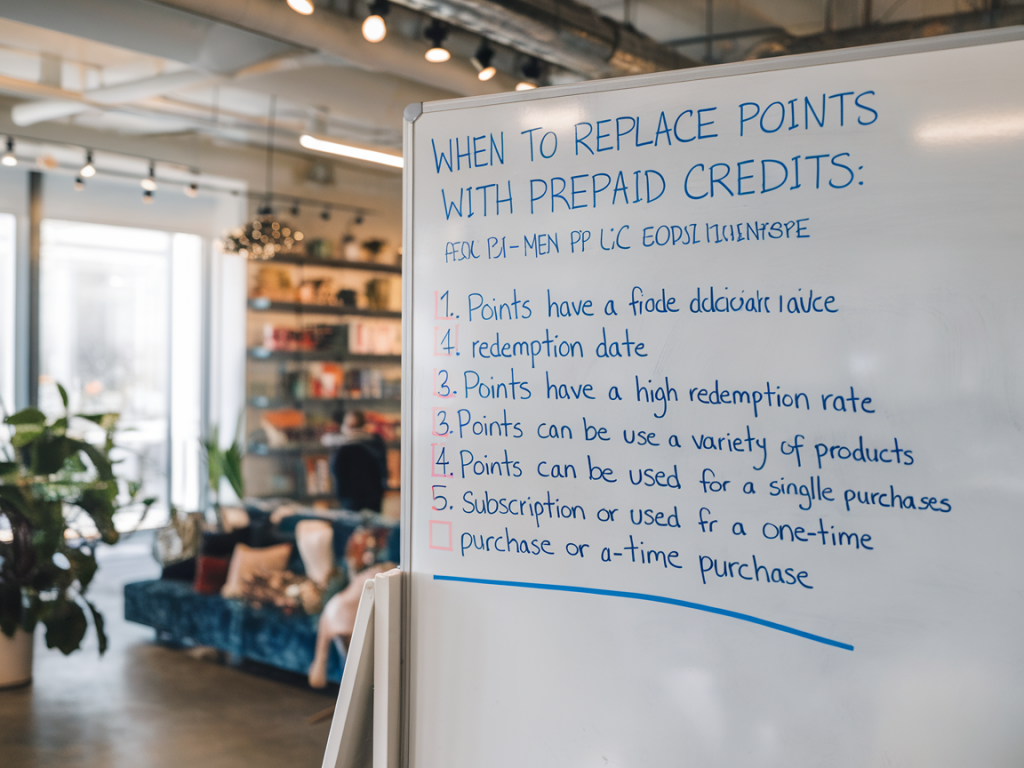

The decision test (three checkpoints)

Run this quick test for each customer segment (new, active, lapsing):

How this applies to subscription businesses

Subscriptions change the calculus because you can influence recurring behaviour more directly.

Practical example: a meal-kit subscription I worked with used a £10 prepaid credit as a churn rescue (offered when customers attempted cancellation). They saw a 25% reduction in immediate churn for those offers, compared with a points-based offer equivalent that had a far lower rescue rate because customers mentally discounted the value.

How this applies to one-time purchase businesses

For e-commerce or retail, the decision hinges on purchase frequency and average order value (AOV).

Case in point: a direct-to-consumer mattress brand introduced a points programme to encourage referrals and content sharing; the points model supported these non-transactional actions better than credits would have.

Operational & UX considerations

Switching currency is not just marketing—it's product, legal and finance work. Key implementation pitfalls I always flag:

KPIs to watch during a trial

Run a time-bound A/B test and track:

| Metric | Credit-favouring signal | Point-favouring signal |

|---|---|---|

| Redemption rate | High (>30%) | Low (<15%) |

| Time-to-redemption | <60 days | >90 days |

| Impact on churn | Immediate reduction | Delayed / long-term uplift |

Final practical tips

If you can’t choose globally, segment. Use prepaid credits for behaviour with short horizons (abandoned carts, cancellation saves, subscription next-bill incentives) and points for long-horizon relationship building (tiers, referrals, status). When migrating, be generous and transparent: customers respond better to a clear conversion with a small bonus than to an unexplained shift.

Changing your loyalty currency is a lever, not a magic bullet. The best outcomes come from matching the currency to the behaviour you need now, instrumenting it with the right KPIs, and being ready to iterate based on real customer response.